If you're the type who manages your own investment portfolio, rebalances your 401(k), and reads financial literature for fun, you've probably mastered the accumulation phase of wealth building. But here's a question that stops most DIY investors in their tracks: what happens to all those carefully constructed portfolios and tax-optimized accounts when you're not around to manage them?

Estate planning probably doesn't give you the same thrill as optimizing your asset allocation or executing a backdoor Roth conversion. But here's the thing: failing to plan your estate properly can undo decades of smart financial decisions in a matter of months.

The good news? As a DIY investor, you already have the analytical mindset needed for effective estate planning. The bad news? Most financial education focuses on accumulation strategies, leaving even sophisticated investors unprepared for wealth transfer planning.

Let's fix that.

Why DIY Investors Often Delay Estate Planning

You understand compound interest, tax-loss harvesting, and the efficient frontier. So why is your estate planning still on the "someday" list?

The complexity paradox: DIY investors often have more complex financial situations precisely because they're sophisticated enough to use multiple strategies. That employer 401(k), your spouse's 403(b), three Roth IRAs (yours, spouse's, and that backdoor conversion account), a taxable account, an HSA you're using as a stealth retirement vehicle, a 529 plan, and maybe some individual stocks you picked up during the pandemic. Each account has different beneficiary designations, tax treatments, and transfer rules.

The "I'm too young" trap: At 45 with $1.5 million in retirement accounts, you're focused on reaching financial independence, not planning for incapacity or death. But estate planning isn't just about death. It's about control, tax efficiency, and protecting your heirs from costly mistakes.

The assumption that simple means adequate: Many DIY investors figure they've covered the basics with beneficiary designations and maybe a will from an online service. Then they're surprised to learn their $800,000 IRA is passed to their heirs in the most tax-inefficient way possible because they didn't understand the rules changed in 2020.

The Foundation: Essential Documents Every DIY Investor Needs

Before we dive into the investment-specific strategies, let's establish the non-negotiables. Think of these as the index funds of estate planning—boring, essential, and surprisingly effective.

The Last Will and Testament

Your will is your instruction manual for asset distribution. For DIY investors, several considerations matter more than for the average person:

Executor selection matters more than you think. You need someone who can handle complexity. That means understanding the difference between your traditional Individual Retirement Account (IRA) and Roth IRA, knowing not to liquidate your taxable account in a single year, and recognizing that your tech company Restricted Stock Units (RSUs) have specific tax implications.

Example: If you appoint your sister who's financially savvy but busy, and your estate includes Incentive Stock Options (ISO), non-qualified stock options, and a traditional brokerage account, will she know which assets to liquidate first to minimize taxes? Will she understand that those inherited retirement accounts now have required distribution timelines?

Asset-specific bequests get tricky fast. Leaving your daughter your brokerage account and your son your IRA sounds equal at $500,000 each, but the tax implications are dramatically different. Your daughter receives a step-up in cost basis on the taxable account (potentially tax-free), while your son faces ordinary income tax on every IRA distribution.

Revocable Living Trust: When It Makes Sense

For DIY investors, a revocable living trust becomes increasingly valuable as your portfolio grows. Here's when to consider one:

You have taxable accounts exceeding $250,000. Trusts allow these assets to bypass probate, which means faster access for your heirs and privacy. Probate is public record. Do you really want everyone in your county knowing the details of your investment portfolio?

You have investment real estate. Rental properties or vacation homes in different states can trigger probate in multiple jurisdictions. A trust consolidates everything under one legal umbrella.

You want control over distribution timing. Maybe you trust your 25-year-old heir completely, but you don't want them inheriting $600,000 in index funds all at once. A trust can stage distributions: say, one-third at 25, one-third at 30, and the remainder at 35.

The trust tax consideration: Revocable living trusts are "disregarded" for tax purposes during your lifetime, meaning they don't create any additional tax compliance burden. Your assets continue to be taxed exactly as they would in your individual name.

Durable Power of Attorney

Here's something most DIY investors miss: who manages your portfolio if you become incapacitated?

Your spouse isn't automatically authorized to manage your individual accounts. If you're hospitalized without a durable power of attorney (POA), your carefully rebalanced portfolio could sit frozen while markets move and opportunities pass.

Financial POA specifics for investors:

- Explicitly grant authority over all investment accounts

- Include language for digital asset access (your brokerage login credentials)

- Consider whether you want immediate authority or "springing" power of attorney (POA) that activates upon incapacity

- Name someone who understands your investment philosophy. They shouldn't panic-sell your equity allocation during a correction

Healthcare Directives

This might seem unrelated to investments, but healthcare costs can devastate even substantial portfolios. Long-term care can cost $100,000+ annually. Your healthcare proxy needs to understand your wishes about life-prolonging treatment, but also should be briefed on your financial situation so they can make informed decisions about care options.

The Investment-Specific Estate Planning Considerations

Now we get to the parts that matter most for DIY investors. These strategies can save your heirs hundreds of thousands in taxes and prevent costly mistakes.

Understanding How Different Assets Transfer to Heirs

Before diving into specific strategies, you need to understand that different account types follow completely different transfer rules. This is where many DIY investors get tripped up—assuming all their accounts work the same way.

| Account Type |

Transfers Via |

Avoids Probate? |

Tax Treatment to Heir |

Key Consideration |

| Traditional IRA/401(k) |

Beneficiary designation |

Yes |

Ordinary income on all distributions |

10-year distribution rule for most heirs |

| Roth IRA |

Beneficiary designation |

Yes |

Completely tax-free |

Best inheritance asset; spend other accounts first |

| Taxable Brokerage |

Beneficiary designation (TOD/POD) or Will |

If TOD/POD: Yes; If Will: No |

Step-up in cost basis eliminates capital gains |

Consider Transfer on Death (TOD) designation |

| Real Estate |

Will, Trust, or Joint Tenancy |

Trust or Joint: Yes; Will: No |

Step-up in basis |

Property in multiple states triggers probate |

| Revocable Trust Assets |

Trust document provisions |

Yes |

Depends on underlying asset type |

Provides privacy and probate avoidance |

| HSA |

Beneficiary designation |

Yes |

Spouse: Remains HSA; Non-spouse: Taxable |

Often overlooked in estate planning |

Critical insight: Notice how beneficiary designations override your will for retirement accounts and can be added to taxable accounts through TOD (Transfer on Death) or POD (Payable on Death) designations. Your will only controls assets that don't have another transfer mechanism, which for most DIY investors is a smaller portion than they realize.

Beneficiary Designations: Your Most Powerful Estate Planning Tool

Here's what shocks most DIY investors: beneficiary designations override your will. You can state in your beautifully drafted will that your IRA goes to your daughter, but if your ex-spouse is still listed as beneficiary from 15 years ago, your ex-spouse gets it.

The per stirpes vs. per capita decision: If you have multiple children and one predeceases you, should their share go to their children (per stirpes) or be redistributed among your surviving children (per capita)? Most DIY investors never consider this until it's too late.

Example: You have three adult children and name them equal beneficiaries per stirpes on your $1.5 million IRA. One child tragically predeceases you but has two young children. Without per stirpes designation, your two surviving children inherit $750,000 each, and your grandchildren receive nothing. With per stirpes, each of your three children's families receives $500,000.

Understanding the SECURE Act Impact on Inherited IRAs

If you created your estate planning before 2020, this is critical: the rules changed dramatically with the Setting Every Community Up for Retirement Enhancement (SECURE Act), and most DIY investors haven't adjusted. For a comprehensive overview of the SECURE Act changes and implementation updates, see our detailed guide on SECURE Act 2.0 implementation.

The old rules (pre-2020): Non-spouse beneficiaries could "stretch" inherited IRA distributions over their lifetime. A 30-year-old inheriting a $500,000 IRA could take small required minimum distributions for 50+ years, allowing decades of continued tax-deferred growth.

The new rules (post-SECURE Act): Most non-spouse beneficiaries must now empty inherited retirement accounts within 10 years. For a high-earning heir, this can create a tax disaster.

Real-world impact: A 40-year-old inheriting a $1 million traditional IRA in a year they're earning $200,000 faces a dilemma. If they withdraw $100,000 annually for 10 years, they're adding $100,000 to their taxable income each year, potentially pushing them into the 35% or 37% federal tax bracket, plus state taxes.

Strategic consideration: This makes Roth conversions during your lifetime more valuable than ever. If you convert traditional IRA assets to Roth while you're in the 24% bracket, your heirs receive tax-free money rather than assets that'll push them into the 35% bracket.

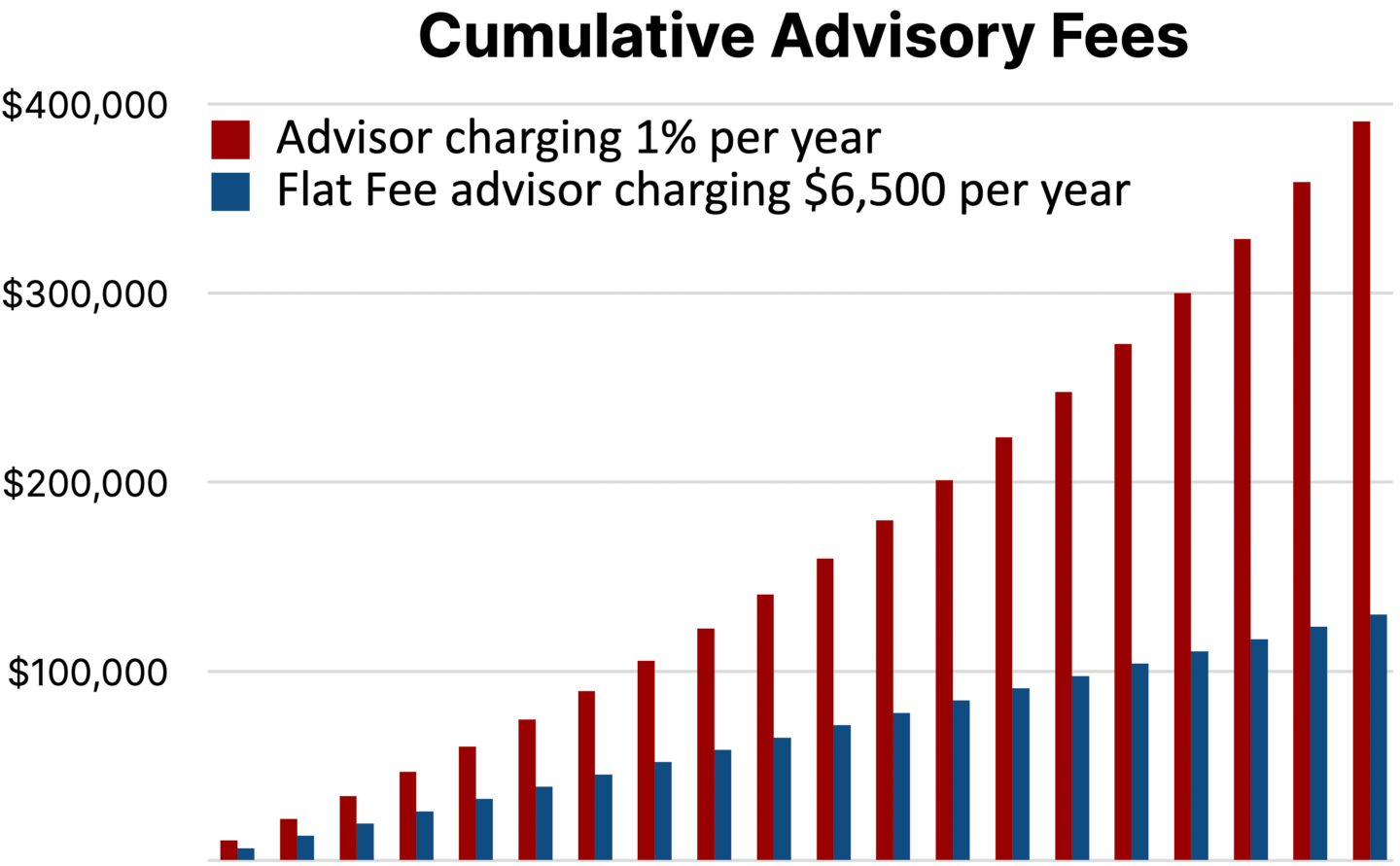

Fee structure note: When evaluating Roth conversion strategies, consider how your advisor gets compensated. Advisors charging a percentage of assets under management (AUM) might be less enthusiastic about conversions that temporarily reduce your taxable account balance (which they manage) to pay conversion taxes. Flat fee advisors can focus purely on the optimal tax strategy for your heirs without worrying about short-term impacts to their fee base.

The Step-Up in Basis Strategy for Taxable Accounts

This is one of the most powerful wealth transfer strategies available, yet many DIY investors don't fully optimize it.

How it works: When you die, your heirs inherit taxable investment accounts at their fair market value on your date of death, eliminating all capital gains accumulated during your lifetime.

Example: You purchased index funds in your taxable account 20 years ago for $200,000. They're now worth $800,000 (a $600,000 gain). If you sold them today, you'd owe long-term capital gains tax on that $600,000 (roughly $120,000 at 20% federal rate). But if you die holding those assets, your heirs inherit them at $800,000 basis with zero capital gains tax owed.

The strategic implication: In retirement, you might want to spend down tax-deferred accounts (traditional IRA, 401(k)) first and preserve taxable accounts for your heirs. This flips the conventional "let tax-deferred accounts grow as long as possible" wisdom on its head.

The concentration risk caveat: If you're sitting on highly appreciated individual stocks (say, $300,000 of employer stock purchased for $50,000), don't let the step-up tail wag the diversification dog. Your heirs would prefer inheriting a diversified $250,000 portfolio over a concentrated $300,000 position in a single stock that could crash.

Retirement Account Distribution Strategy

Different retirement accounts have different optimal uses in estate planning.

Roth IRAs: The superior inheritance asset

- Tax-free to beneficiaries

- No required minimum distributions during your lifetime

- Even under the 10-year rule, all distributions remain tax-free

- Strategy: Spend traditional IRA/401k assets first, preserve Roth for heirs

Traditional IRAs/401(k)s: Plan for the tax hit

- Every distribution is ordinary income to beneficiaries

- Can push heirs into higher tax brackets

- Strategy: Consider strategic Roth conversions during low-income years (early retirement, business loss years)

The spouse vs. non-spouse beneficiary rules: Spouses have unique options. They can treat an inherited IRA as their own, roll it into their existing IRA, or maintain it as an inherited IRA. Non-spouse beneficiaries have fewer options and generally face the 10-year distribution rule.

Scenario: You're 58, semi-retired, earning $80,000 annually, with a $600,000 traditional IRA. You're in the 22% tax bracket with plenty of room before hitting the 24% bracket threshold. This is prime Roth conversion territory—convert $50,000 annually for several years, paying 22% tax now, so your heirs receive tax-free Roth assets instead of traditional IRA assets they'd pay 32% or 35% tax on during their peak earning years.

Charitable Giving Strategies for DIY Investors

If you're charitably inclined, integrating giving into your estate planning can provide significant tax benefits.

Qualified Charitable Distributions (QCDs): Once you're 70½, you can donate up to $108,000 annually (2025 limit) directly from your IRA to qualified charities. This satisfies your required minimum distribution (RMD) without increasing your taxable income.

Strategy value: If you don't need your RMDs for living expenses, QCDs provide tax savings over taking the distribution and then donating cash, especially after the increased standard deduction makes itemizing less common.

Donor-Advised Funds (DAFs): These are like charitable investment accounts. You contribute appreciated securities, get an immediate tax deduction, and recommend grants to charities over time. For DIY investors, DAFs offer portfolio control—you can often direct the investment allocation of assets within the DAF.

Charitable remainder trusts for concentrated positions: If you're sitting on highly appreciated stock (think early Amazon employee with $2 million in Amazon shares purchased for $40,000), a charitable remainder trust lets you donate the shares, receive income for life, avoid immediate capital gains tax, and eventually benefit charity. This is complex territory that requires professional guidance, but for specific situations, it's remarkably effective.

Common Estate Planning Mistakes DIY Investors Make

You've mastered dollar-cost averaging and tax-loss harvesting, but these estate planning mistakes trip up even sophisticated investors.

Mistake #1: Forgetting about asset titling

Your will says your taxable brokerage account goes to your children equally, but the account is titled "Joint Tenant with Rights of Survivorship" with your spouse. Your spouse automatically owns it when you die, your will is irrelevant for that account.

Mistake #2: Naming your estate as IRA beneficiary

If no individual beneficiary is named in your IRA, it defaults to your estate. This is almost always suboptimal. It triggers immediate taxation, accelerates the distribution timeline, and creates probate complications.

Mistake #3: Not coordinating beneficiary designations with overall estate plan

Here's where advisor compensation structures can create blind spots. If you're working with an AUM advisor who only manages part of your assets, they might not have full visibility into (or frankly, financial incentive to optimize) accounts held elsewhere. Your company 401(k) with $800,000 might have outdated beneficiaries because it doesn't contribute to their annual fee. Comprehensive planning requires someone looking at your complete picture, regardless of where assets are held.

Mistake #4: Not considering the tax situation of heirs

Leaving equal dollar amounts sounds fair, but leaving $500,000 in Roth IRA to one heir and $500,000 in traditional IRA to another creates dramatically different after-tax inheritances.

Mistake #5: Ignoring state estate taxes

The federal estate tax exemption is $13.99 million for 2025 ($27.98 million for married couples), so most DIY investors don't worry about federal estate tax. But several states have much lower thresholds than the federal exemption. For example, Oregon's exemption is around $1 million, while Massachusetts' estate rules now effectively exempt estates of $2 million or less after recent state law changes. If you live in one of these states with a $2 million portfolio, state estate tax planning might be necessary.

Mistake #6: Using online documents without professional review

LegalZoom templates might work fine for simple situations, but DIY investors usually don't have simple situations. Those three IRAs, the 401(k) with different beneficiaries, the taxable account, the rental property: all of this creates complexity that generic documents miss.

When the DIY Investor Should Hire Professional Help

You're comfortable managing your own portfolio, so when do you need to bring in estate planning professionals?

Trigger points suggesting professional help:

- Net worth exceeding $1 million

- Multiple types of retirement accounts requiring coordination

- Appreciated assets creating significant capital gains exposure

- Blended family situations requiring specific distribution strategies

- Minor children or heirs with special needs

- Business ownership or complex compensation (ISO, RSU, Employee Stock Purchase Plan)

- Assets in multiple states

- Charitable giving as part of legacy planning

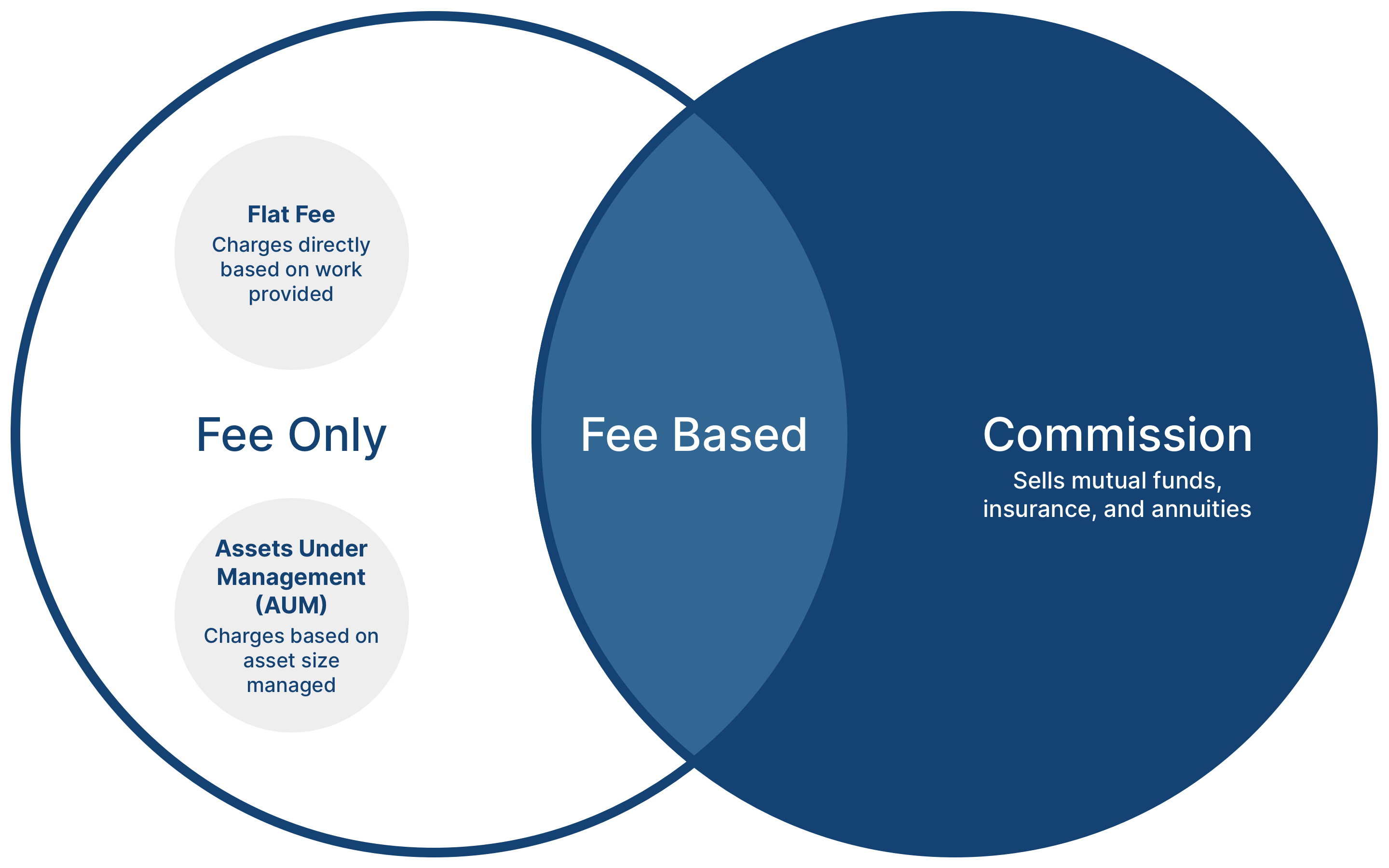

The fee structure consideration: Just as you prefer index funds over active management for their lower costs and transparency, consider estate planning professionals who charge flat fees for document preparation rather than percentage-based fees or AUM fees. You want someone focused on creating the optimal plan for your situation, not maximizing assets under management.

Estate planning typically requires intensive work upfront, then periodic updates—a fee structure that naturally aligns with flat fee or project-based pricing. An advisor charging based on AUM might encourage you to keep all assets in accounts they manage (even if your employer's 401(k) offers better options) simply because it increases their ongoing revenue. When estate planning intersects with investment strategy—which it always does for DIY investors—compensation alignment matters.

The Bottom Line

You've spent years building wealth through disciplined saving, smart investing, and tax optimization. Don't let poor estate planning undo those gains.

Estate planning for DIY investors isn't about creating complicated trusts or exotic strategies (though those sometimes have their place). It's about ensuring your carefully constructed portfolio passes to your heirs efficiently, minimizes taxes, and prevents costly mistakes.

The analytical skills that make you a successful DIY investor, attention to detail, tax awareness, long-term thinking, are exactly what's needed for effective estate planning. You don't need to become an estate planning expert, but you do need to apply the same rigor to wealth transfer that you apply to wealth accumulation.

Start with the basics: update those beneficiary designations, create essential documents, and understand how different account types transfer to heirs. Then layer in the optimization strategies: Roth conversions, asset location for step-up basis, and distribution planning.

Your heirs will thank you. More importantly, you'll have the peace of mind that comes from knowing your financial legacy is protected.

Up Next

Earning $500,000+ should mean financial freedom, right? Yet many high-income professionals find themselves living paycheck to paycheck despite substantial earnings. In "Why $500K Earners Still Live Paycheck to Paycheck," we expose how lifestyle inflation quietly consumes income growth and why top earners often accumulate wealth slower than colleagues earning half as much. You'll see the actual math behind where a $500,000 income disappears, understand why high earners are particularly vulnerable to lifestyle creep, and discover practical strategies to break free, including how your advisor's fee structure might be making the problem worse.

Sources and References

- Internal Revenue Service. "IRS provides tax inflation adjustments for tax year 2025." October 22, 2024.

- Internal Revenue Service. "Retirement Topics - Beneficiary."

- Congress.gov. "H.R.1994 - Setting Every Community Up for Retirement Enhancement Act of 2019."

- American Bar Association. "Estate Planning Info & FAQs."

- The Tax Foundation. "Estate and Inheritance Taxes by State, 2024." November 12, 2024.

- Fidelity. "Required Minimum Distributions (RMDs): What You Need to Know."

- Vanguard. “What to do with an inherited IRA.”

- DALBAR, Inc. "Quantitative Analysis of Investor Behavior (QAIB)."

- Morningstar. “Inherited IRAs: What to Know About Taxes, RMDs, and More.” September 29, 2025.

- Journal of Accountancy. “The SECURE Act’s changes.” July 1, 2020.

- Kitces, Michael. "New SECURE Act Stretch IRA Rules For Eligible Designated Beneficiaries." February 12, 2020.

- Financial Planning Association. "Estate Planning Update." April 2020.